One of West Africa’s richest men and a formidable force in banking, Jim Ovia conveys some key lessons for Africa’s entrepreneurs in his first book.

In Africa’s business and banking world, a man like Jim Ovia is a textbook case study.

As the founder and chairman of Zenith Bank, and with a net worth of $825 million according to FORBES, Ovia’s prolific banking career spans almost three decades.

His book, Africa Rise and Shine: How a Nigerian Entrepreneur From Humble Beginnings Grew A Business To $16 Billion, launched in August, which marked his debut as an author, details this trajectory, building the bank from the ground up, brick-by-brick. Ovia started with a single branch in Lagos on the ground floor of an impoverished residential duplex that he shared with a private tenant.

“At the time, there were no high-rise office structures in the area and we were not able to afford any standalone structures,” says Ovia to FORBES AFRICA when we meet him at the iconic Civic Centre building located on Ozumba Mbadiwe in Victoria Island, Lagos.

The sprawling high-rise office structure we occupy on this rainy Saturday morning is a far cry from the early years.

Ovia recalls erecting a signage and the company logo in the impromptu commercial space where they could carry out the banking business.

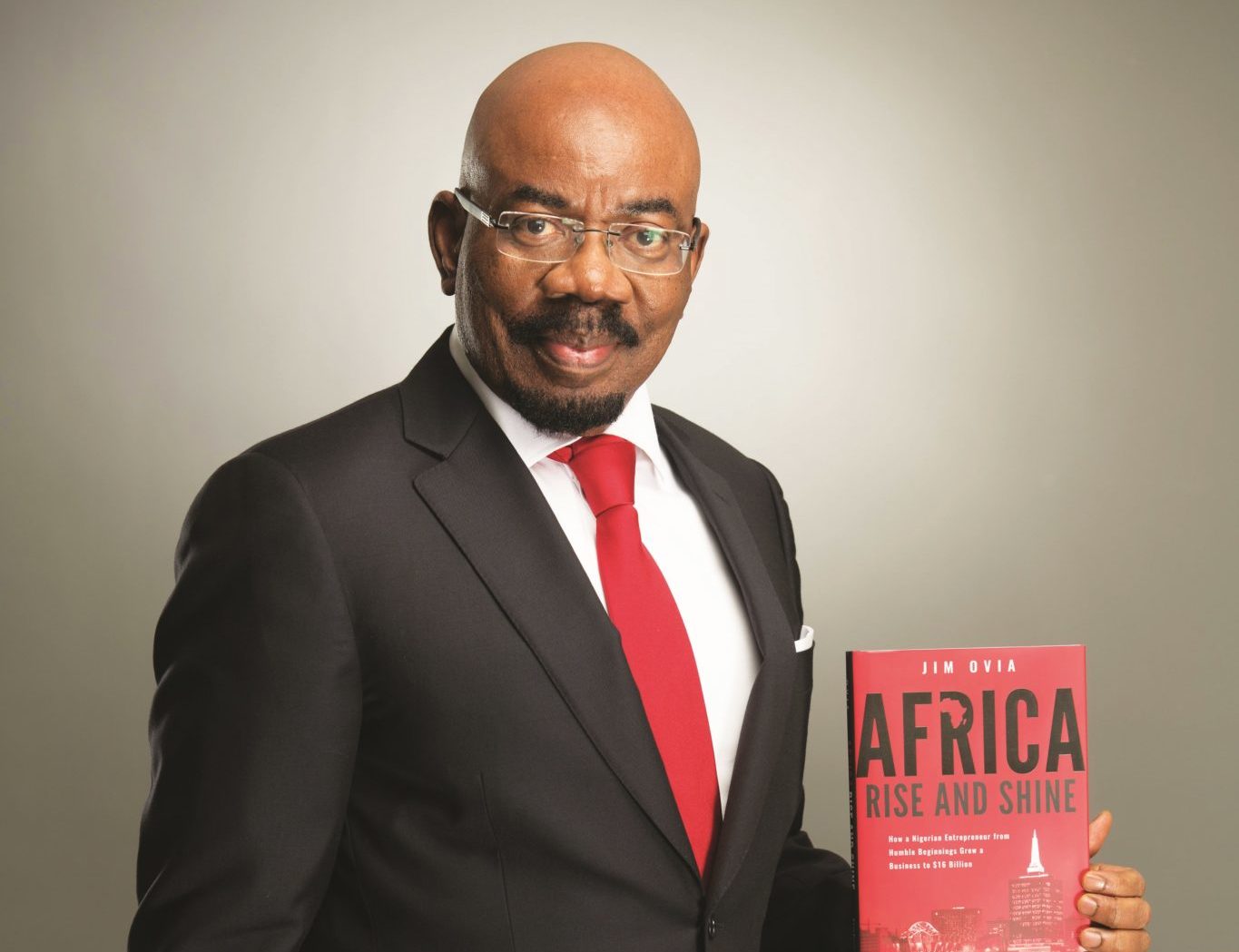

Photo by: Kelechi Amadi-Obi

He worked at Barclays Bank in Lagos from the age of 18 for three years as a clerical officer before enrolling to study business administration at Southern University, Louisiana, in the United States, and subsequently proceeding to the University of Louisiana, Monroe, where he completed his MBA.

After graduating, he joined Union Bank to complete his National Youth Service Corps (NYSC). Ovia subsequently joined the Merchant Bank of Africa, which was then owned by Bank of America, and worked for over three years before applying for a banking license. And with that, came the birth of Zenith Bank.

“We knew it was going to be a bank that was well run. We knew it will be a bank that will be very efficient and we knew it will be a bank that will offer good and excellent service because that is one of the reasons we set up the bank in the first place,” recalls Ovia.

From those days, he had decided Zenith was going to be run differently from any other bank.

“When you go to many Zenith Bank offices, you will still not see any crowds in the banking hall, yet we are still providing the best quality service,” says Ovia.

The banking major is a London Stock Exchange-listed company with operations in the UK, China, the UAE, Ghana, Gambia, Sierra Leone, and with more than 400 branches and business offices in Nigeria.

The institution has become a byword for credibility in the Nigerian banking industry.

Many of his peers and competitors call the Zenith Bank success story one of hard work, grit and focus.

But what distinguishes Ovia from them is an abiding belief in his entrepreneurial instincts, one that has been validated many times over.

But that is not the reason he has a spring in his step these days. In Ovia’s new chapter as an author, he chronicles the key lessons entrepreneurs can learn from the meteoric rise of Zenith Bank.

“Among the most important of those lessons may be my experience that it is not necessary to be born rich or in influential circles in order to achieve success,” says Ovia.

It augurs well for a man who for 30 years has constantly adapted to changing environments and opportunities, whether it was being an early investor in the internet space, through his company Cyberspace in 1995, or setting up his telecommunications company Visafone and his expansive real estate portfolio. Ovia’s intuitive timing is something a lot of Nigerian entrepreneurs who look up to him as a mentor have been reading about in his book.

Says Richard Branson, founder of the Virgin Group, in a blurb on the back of the book: “Jim Ovia’s entrepreneurial flair demystifies Africa. Africa Rise and Shine shows his meteoric rise from humble beginnings to building a formidable bank. This is a wonderful African success story,”

Africa’s richest man Aliko Dangote, founder and president, Dangote Group, also echoes those sentiments.

“Jim Ovia has been my friend and a trusted banker over the last twenty-five years. Africa Rise and Shine lays bare the secrets to Zenith Bank’s success from one of Nigeria’s most respected businessmen. Jim’s inspirational tale of success against all the odds is an important lesson of how adversity can always be surmounted. His principles of doing business can be applied globally as demonstrated by Zenith Bank’s London Stock Exchange listing. This book is an essential read for anyone that wants to do business in Africa.”

Ovia believes it is imperative to rely on one’s own instincts in taking stock of one’s capabilities, and in evaluating new business opportunities.

READ MORE: The Nigerian Who Runs His Business On Luck

The book seeks to encourage entrepreneurs to seize the opportunity to invest in Africa by abiding by guidelines such as prudence, due diligence and being able to respond quickly by cultivating the capacity to react effectively.

“I think the readers of this book will gain the spirit of commitment, empowerment, focus, hard work and discipline. They will learn that if you are disciplined and work hard, definitely you will do well. The book is about passing on these principles and documenting how it is to do business in Africa, particularly Nigeria,” says Ovia.

He hopes his book, which is more like an entrepreneurs’ manual than an autobiography, will guide the next generation of industrialists and game-changers to change the narrative of Africa from a hopeless continent to a rising continent.

From boardroom deal-making to creating an impact in the lives of Nigerians, Ovia is a business icon who continues to evolve.

His book is a call to tomorrow’s titans to follow their gut instincts, so hopefully one day, they too can reach their zenith.